portability estate tax exemption

Ad Practical And Affordable CPE Courses For CPAs. Portability helps minimize federal gift and estate taxes by allowing a surviving spouse to use a deceased spouses unused gift and estate tax exemption amount.

Tax Related Estate Planning Lee Kiefer Park

When one spouse outlives the other this widow or widower may utilize the unused tax exemption from the deceased spouse to reduce the tax liability on the estate of the surviving spouse.

. Lets say Spouse A dies in 2022 when the estate tax exemption is 1206 million. On July 8 2022 the Internal Revenue Service issued new guidance that allows a deceased persons estate to elect portability of their unused gift and estate tax exemption for up to five years after their death. How do I Elect Portability.

Back to the example above and assuming the current federal gift and estate tax exemption is in fact reduced by half in 2026 if portability is elected and the surviving spouse dies in 2027 the 506 million of unused gift and estate tax exemption for the Deceased Spouse will be added to the 603 million gift and estate tax exemption for the. But you must file an estate tax return for your spouse and complete the section of Form 706 currently entitled portability of deceased spousal unused exclusion Now Is a Good Time to Consider If You Could Benefit from Portability. Subscribe And Save More At CPA Self Study Online.

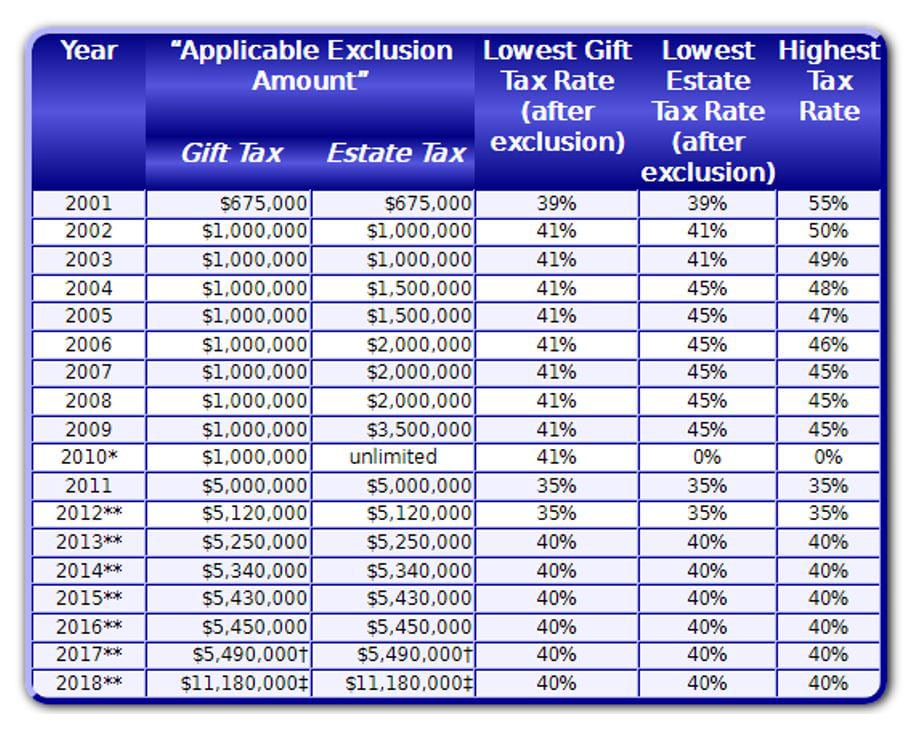

Portability of the estate tax exemption means that if one spouse dies and does not make full use of his or her 5000000 in 2011 or 5120000 in 2012 5250000 in 2013 5340000 in 2014 and 5430000 in 2015 federal estate tax exemption then the surviving spouse can make an election to pick up the unused exemption and add it to the. To secure the portability of the first spouses unused exemption the estate executor must file an estate tax return even if the estate is exempt from filing a return because no tax is due. Portability of the Estate Tax Exemption.

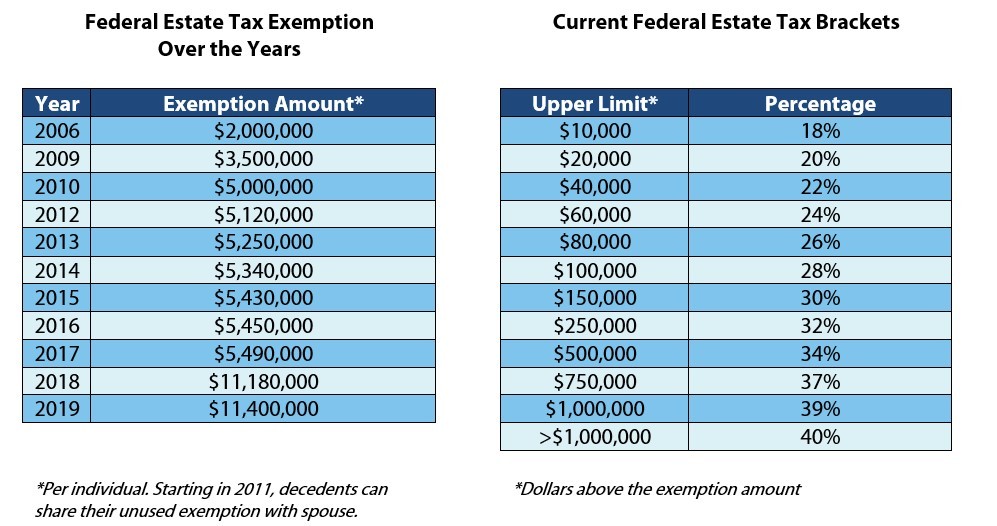

It allows the spouses to go about their estate planning and transfer assets upon their death the way that they would like to to carry out their wishes. In 2012 inflation adjustments increased the exemption to 5120000. The key advantage of portability is flexibility.

In this example that is nearly 8 million. The Tax Cuts and Jobs Act increased the federal estate tax exemption in 2018 and it has increased since then adjusting with inflation so its no surprise that the exemption is higher for 2022. The Internal Revenue Services allows for estate and gift tax portability.

After all electing portability could mean that a surviving spouse could have double the estate tax exemption at the second death currently 5430000 x 2 10860000. Please note these laws being permanent means that they are not set. Portability also applies to gift tax and therefore the gift tax exemption is also 16880000 for the survivor.

So if your spouse passed away less than five years ago you may be able to file an. In order to benefit from this exemption however the surviving spouse must file IRS Form 706 the United States Estate and Generation-Skipping Transfer tax return within nine months of the first death in order to elect portability. Some lawmakers have proposed lowering the amount even.

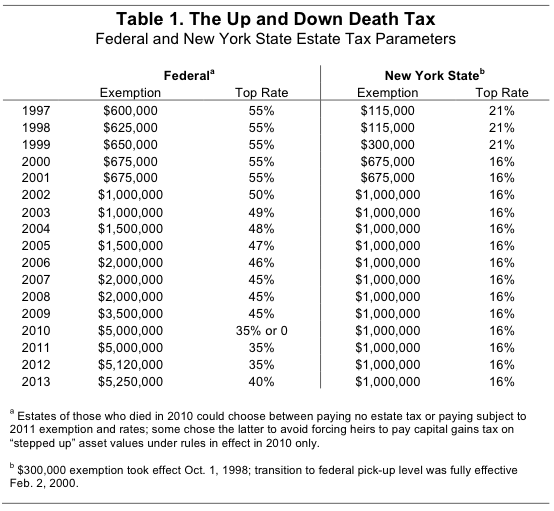

And then after one spouses death then the surviving spouse can take steps to combine their estate tax exemptions to reduce estate tax. The federal estate tax exemption is indexed for inflation so it increases periodically usually yearly. We waited a long time many would say too long for estate tax legislation and when it arrived in December 2010 it provided some surprisesPerhaps the most significant surprise is the addition of portability of estate and gift tax exemptions between spouses which had been included in prior bills but was not anticipated to be part of the compromise package.

At a tax rate of 40 they have to pay more than 3 million in taxes to. Typically portability estate tax allows an executor to act on behalf of the deceased spouse to exercise the options available for estate tax exemption amount that remained unused at the time of death of a taxpayer. Therefore the objective should be to get the survivors estate at or below the 4000000 threshold for Illinois.

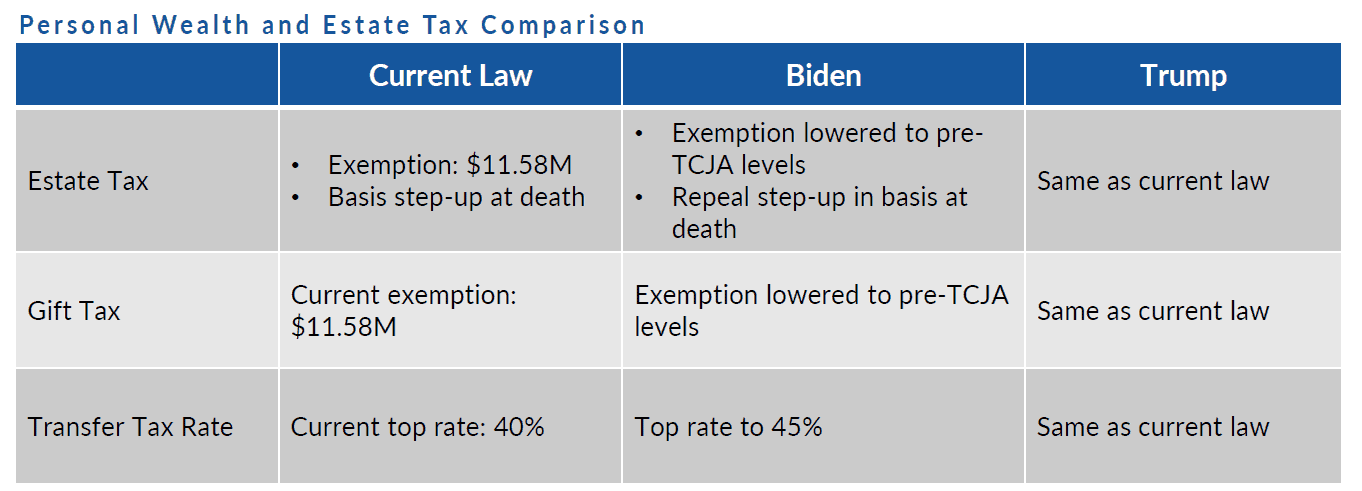

The current federal gift and estate tax exemption will be reduced by half in 2026. If during hisher lifetime the survivor. Regarding the estate tax exemption for couples.

However the exemption is scheduled to drop to 1 million after 2012 unless Congress intervenes. The American Taxpayer Relief Act of 2012 ATRA made permanent the portability of estate tax exemption between spouses. The Illinois estate tax on an estate of 16880000 would be 1524400.

Please note that these exemption amounts are for individuals. It sat at 114 million for 2019 1158 million for 2020 and it has now hit 117 million for 2021. If during Spouse As lifetime they had only used 1 million of their exemption amount Surviving Spouse B may elect portability to claim 1106 million DSUE as long as they file for the exemption within five years of the decedents date of death.

With exemption levels being indexed for inflation the exemption amount has gone up still. 247 Access To More Than 130 Courses. IRS expands portability of a 2412 million estate tax exemption but things may change dramatically in 2026.

By Natasha Meruelo. This essentially means spouses can combine their estate and gift tax exemptions. This was just the estate tax portability rules though.

The Tax Relief Unemployment Insurance Reauthorization and Job Creation Act of 2010 exempts from federal estate tax the first 5 million of a decedents taxable estate. By continuing to browse or by clicking Accept All Cookies you agree to the storing of first- and third-party cookies on your device to enhance site navigation analyze site usage and assist in our marketing efforts. Without portability they will pay taxes on the difference between the value of your estate and the current estate tax exemption.

With the current estate tax exemption now at 1206 million for an individual most people will. Asking the portability question. The tax exemption change works with the federal gift and estate tax where the TCJA act doubles the existing exemption from 5.

Under portability if the first spouse to die does not use his or her exemption from estate and gift tax the executor of the first spouses estate may elect to give the use of the. Learn With CPA Self Study. Portability allows a surviving spouse the ability to transfer the deceased spouses unused exemption amount DSUEA for estate and gifts taxes to a surviving spouse so long as the Portability election is made on a timely filed federal estate tax return IRS Form 706.

After 2012 one important question for estate planning is whether or not portability should be elected at the first death. This estate tax return is a Form 706. To elect portability the executor or personal representative of the estate must file an estate tax return on or before the fifth anniversary of the decedents date of death.

It is twice the amount for married couples. Currently the exemption is 1206 million but its scheduled to return to an inflation-adjusted 5 million on January 1 2026. As of that time the estate tax exemption was much lower.

Save Our Homes

How Changes To Portability Of The Estate Tax Exemption May Impact You

Adler Adler Portability Of Estate Tax Exemption

What Surviving Spouses Need To Know About The Marital Portability Election Natural Bridges Financial Advisors

The Federal Gift Tax Applies Whenever You Give Someone Other Than Your Spouse A Gift Worth More Than 15 000 Tuition Payment Federal Income Tax Tax

19703 Jpg

Portability Of Unused Estate And Gift Tax Exclusion Between Spouses

Historical Estate Tax Exemption Amounts And Tax Rates 2022

Estate Planning Technique Grantor Retained Annuity Trusts C W O Conner Wealth Advisors Inc Atlanta Georgia

Historical Estate Tax Exemption Amounts And Tax Rates 2022

What Spouses Need To Know About Portability Of The Estate Tax Exemption

What Is Portability For Estate And Gift Tax Portability Of The Estate Tax Exemption The American College Of Trust And Estate Counsel

Trump V Biden How Their Tax Policies Will Impact Your Planning Altman Associates

Exploring The Estate Tax Part 2 Journal Of Accountancy

Irs Announces 2017 Estate And Gift Tax Limits The 11 Million Tax Break

New York S Death Tax The Case For Killing It Empire Center For Public Policy

Portability Of A Deceased Spouse S Unused Exemption

Power Of Portability This Estate Tax Tool Can Save You Millions Agweb

Understanding Qualified Domestic Trusts And Portability